Buying your first home in London can feel out of reach. The average first property in the capital now costs more than £500,000, a level it passed for the first time during 2026. Saving a deposit while paying rent, decoding stamp duty, and choosing the right borough all pile on the pressure.

Yet thousands of people still take that leap every year, and most of them started exactly where you are today. Following London property news and advice from agents who watch the market daily helps you spot value before others do. This guide breaks the whole journey into clear stages, from your opening savings target to picking up the keys.

Key Takeaways

- A typical London first home now tops £500,000, so plan your deposit and borrowing early.

- No stamp duty applies below £300,000, yet the relief vanishes once a price climbs past £500,000.

- A Lifetime ISA adds a 25% government top-up, though its £450,000 ceiling rarely fits central districts.

- Schemes such as Shared Ownership and a 95% mortgage guarantee open doors on a smaller deposit.

- A local estate agent shortens your search and steadies you through every legal stage.

How Much a First Home in the Capital Really Costs

London property prices sit far above the national average, which shapes everything about your first purchase. The average first-time buyer home across the capital passed £500,000 during 2026, while the wider UK figure stood at around £254,750. That gap explains why a deposit here stretches much further than it does across most regions.

Mortgage rates weigh heavily too. The cost of a typical five year fixed deal rose from roughly 4% to about 5% through 2026, which lifts monthly repayments on every loan. Most first homes in the capital are leasehold flats, so factor service charges and ground rent into your sums as well. Set aside a small contingency buffer as well, because moving dates slip and early repairs have a habit of appearing.

| Key figure: London’s average first home crossed the £500,000 line for the first time in 2026, roughly £15,000 higher than a year earlier. |

A clear picture of the upfront bill keeps nasty surprises away. Here is what most buyers budget for:

| Cost | What it covers | Typical London range |

|---|---|---|

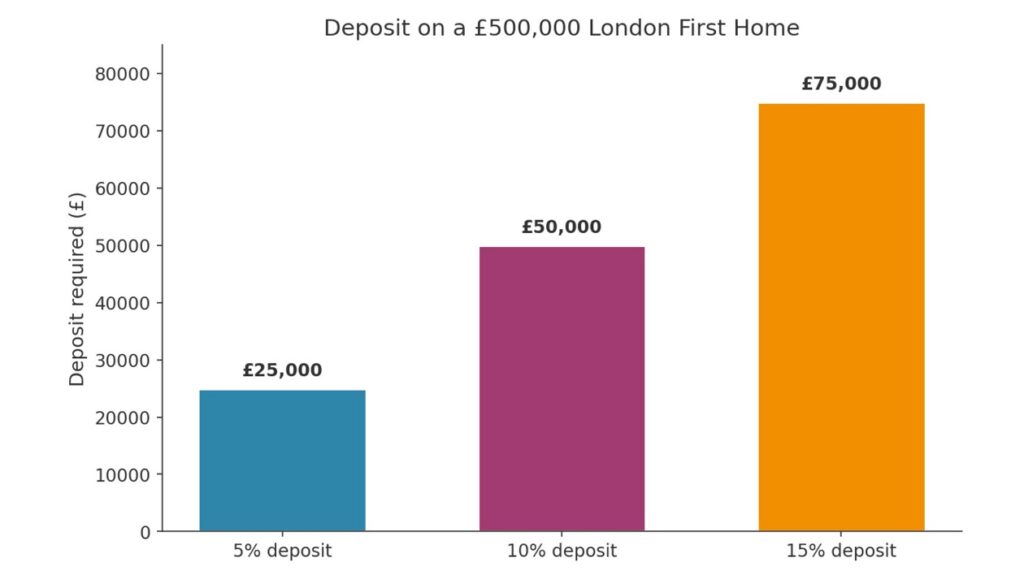

| Deposit | Your share of the purchase price | £25,000 to £75,000 |

| Stamp duty | Tax on the purchase | £0 to £17,500 |

| Legal and conveyancing | Solicitor handling the sale | £1,500 to £3,000 |

| Survey | Condition check on the home | £400 to £1,500 |

| Mortgage and valuation fees | Lender arrangement costs | £0 to £2,000 |

| Removals | Moving your belongings | £400 to £1,200 |

Table 1: Typical upfront costs for first-time buyers in London.

Saving a Deposit That Goes Further

A deposit is the single biggest hurdle for most buyers entering the London market. Lenders accept as little as 5% of the price, yet putting down a tenth usually unlocks sharper interest rates and a wider product choice. On a £500,000 flat, that is the difference between finding £25,000 and £50,000.

Your borrowing has a ceiling too. Most lenders offer around 4.5 times your income, so two salaries often make the sums work in the capital. A gift from family, sometimes called the bank of mum and dad, remains a common way to reach the target faster.

A Lifetime ISA can speed things along. Under the government Lifetime ISA rules, savers aged 18 to 39 may pay in up to £4,000 each tax year and receive a quarter on top as a bonus worth up to £1,000.

| Tip: Pay in the full £4,000 a year and the state adds £1,000. Across five years that is £5,000 of free money working towards your first home. |

The snag for Londoners is the price ceiling. This account only works on a first home costing £450,000 or below, which sits under the city average. Buy above that level and you face a withdrawal charge that claws back the bonus along with a slice of your own savings.

A Lifetime ISA only covers a first home priced at £450,000 or less, a ceiling that has stayed frozen since 2017.

Stamp Duty for First-Time Buyers in London

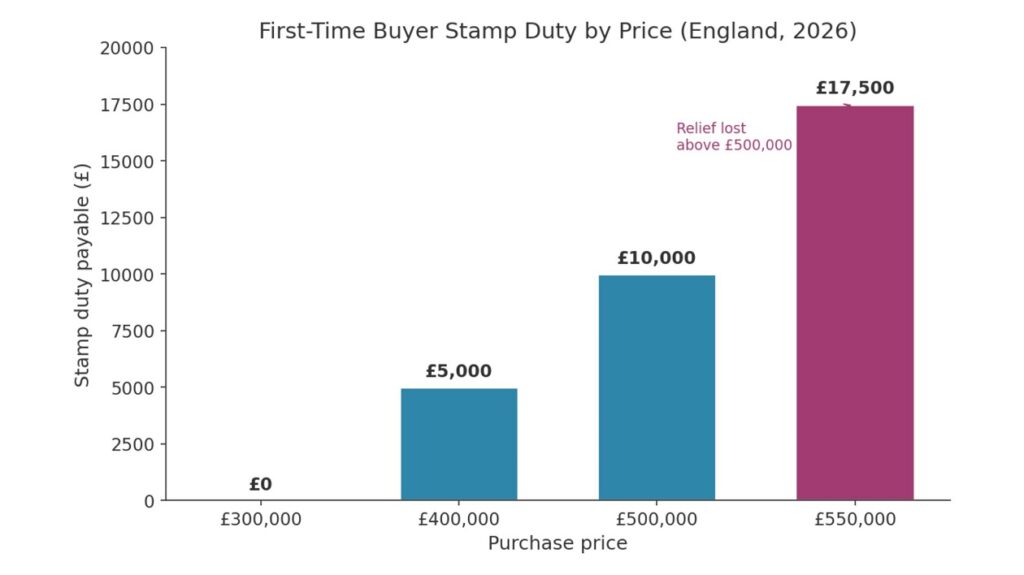

First-time buyers owe no stamp duty on the first £300,000 of a home, then 5% on any value between £300,001 and £500,000. Once the price tops £500,000 the relief disappears, and standard rates apply to the entire amount. Thresholds reverted to these figures on 1 April 2025, and you can confirm the current Stamp Duty Land Tax rates on the government website.

The cliff edge at half a million catches many capital buyers off guard.

| Portion of the price | First-time buyer rate |

|---|---|

| Up to £300,000 | 0% |

| £300,001 to £500,000 | 5% |

| Over £500,000 | No relief; standard rates apply to the whole price |

Table 2: First-time buyer stamp duty bands in England (2026).

| Warning: A first home priced at £500,000 carries £10,000 in tax, but one at £550,000 jumps to £17,500 because the discount is lost completely. A modest difference in asking price can cost thousands. |

Government Schemes That Can Help

A range of government schemes exist to bridge the gap between high prices and modest savings. The Help to Buy equity loan has closed to new applicants, so your attention should sit on the routes still running today.

The Mortgage Guarantee Scheme

This scheme encourages lenders to offer 95% mortgages by covering part of their risk. Now a permanent programme, it supports homes worth up to £600,000, letting buyers move with just 5% down.

Shared Ownership

Shared Ownership lets you buy a portion of a property, often between 10% and 75%, and pay rent on the remainder to a housing association. Your deposit reflects only the share you purchase, which lowers the entry cost sharply and suits tighter budgets.

The First Homes Scheme

This route offers selected new builds at a discount of at least 30% off market value. In the capital the discounted price cannot exceed £420,000, and a household income must stay under £90,000 to qualify.

| Scheme | How it helps | Key London limit |

|---|---|---|

| Mortgage Guarantee Scheme | 95% mortgage with a 5% deposit | Home worth up to £600,000 |

| Shared Ownership | Buy a share, rent the rest | Deposit based on the share bought |

| First Homes Scheme | 30% or more off a new build | Discounted price up to £420,000; income under £90,000 |

Table 3: Live schemes that lower the cost of a first home in London.

The Buying Process Step by Step

The buying journey in London follows the same path as the rest of England, though competition tends to move faster. Knowing each stage in advance helps you act with confidence when the right home appears.

- Work out your budget and secure a mortgage agreement in principle.

- Register with agents, then view homes that fit your shortlist.

- Make an offer and negotiate on price.

- Appoint a solicitor or licensed conveyancer to handle the legal work.

- Arrange a survey and let your lender value the property.

- Receive your formal mortgage offer.

- Exchange contracts, the point at which the deal becomes binding.

- Complete the purchase, transfer the money, and collect your keys.

Strong local knowledge keeps the experience calm. One recent Google reviewer, Samuel C., praised Goldwyn Knight for steady guidance throughout, crediting the team insight into the area and its values for giving him solid footing from day one. That kind of steer matters most when you buy for the very first time.

The legal side of a property purchase can feel dense, so a sharp solicitor and careful reading make a real difference.

Choosing the Right Area

Location decides both your budget and your daily life across the capital. Outer boroughs and pockets of South London give first-time buyers more space for the money, while strong rail and Tube links keep the centre within reach. Greenwich, Charlton, and Blackheath draw buyers who want value without losing their connection to town.

Look beyond the asking price. Energy bills, council tax, and travel all shape what you can truly afford, so weigh the running costs of a home next to the mortgage itself. Check which travel zone a home sits in, since a single zone shift can change your annual commute cost noticeably.

After you collect the keys, small upgrades can lift both comfort and resale value over time. If you prefer to study each step in depth, practical how-to guides can walk you through the paperwork.

Frequently Asked Questions

How much deposit do I need to buy in London?

Most lenders will accept a deposit of 5%, so a £500,000 purchase needs at least £25,000. Raising that to a tenth, around £50,000, usually secures lower rates and a broader choice of mortgage deals.

Who qualifies for first-time buyer status?

Anyone who has never owned or inherited a residential property anywhere in the world. When you buy jointly, every applicant must meet that definition to claim the relief or use most support schemes.

Do first-time buyers pay stamp duty in London?

Plenty do. Nothing is due below the £300,000 line, then a 5% charge applies up to half a million. Because the average capital home tops that figure, many buyers lose relief and pay full rates.

Is a Lifetime ISA worth it for London buyers?

It can be, provided your target home stays at or below £450,000. The bonus lifts your deposit, yet a purchase above the cap triggers a penalty, so check local prices before you lean on it.

How long does buying a home take?

From accepted offer to completion usually runs two to four months in the capital, though chains, surveys, and lender checks can stretch it. Sorting your finances early keeps delays short.

Should I use a mortgage broker?

A broker compares deals across many lenders and can pinpoint products suited to a smaller deposit or complex income. The fee is often offset by a keener rate, which makes the help worthwhile for plenty of first-time buyers.

Final Thoughts

Becoming a homeowner in London asks for patience, planning, and a clear view of the numbers. Once you grasp your deposit, your stamp duty position, and the schemes open to you, the capital starts to feel far less daunting. Line up your money, lean on people who know the streets you hope to live on, and move at a pace that suits your circumstances. The keys to your own front door are closer than the headlines suggest.

{kind=link}